One of the most common things I hear in my office is:

“Ilir, I owe the IRS more than I can pay. What do I do?”

First thing don’t panic.

I’ve been doing tax resolution work for more than 20 years, and if there is one thing I have learned, it is that most people spend months, and sometimes years, worrying about the IRS before they ever sit down and find out what their options are.

I have had people come into my office with grocery bags full of IRS notices. I’m not kidding. Grocery bags. They haven’t opened them because they fear what might be inside. Some have not opened a letter in months. Others have ignored the problem for years because they believe there is no solution.

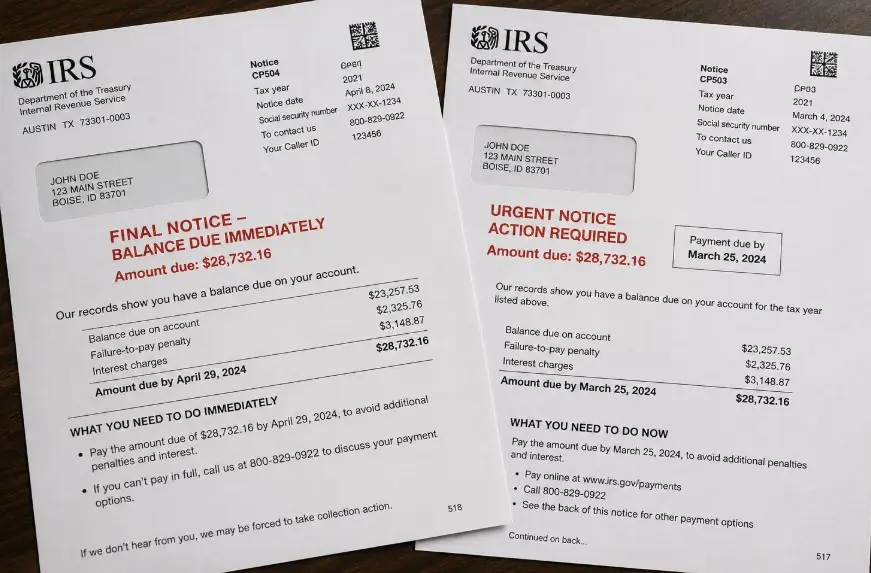

The problem is that the IRS keeps working whether you open the letters or not. Interest keeps running. Penalties keep running. The notices keep coming.

So the worst thing you can do is absolutely nothing.

Over the years, I’ve sat across the table from people in Boise, Meridian, Eagle, Garden City, Kuna, Nampa, Caldwell, Twin Falls, Idaho Falls, and just about every corner of Idaho. The story is rarely the same, but the feeling usually is.

Business had a couple of rough years, A spouse got sick., A divorce changed everything.

A taxpayer took money out of retirement thinking they would catch up later.

Then life happened.

Before they know it, they owe the IRS far more than they ever imagined.

What surprises me is how many people spend years worrying about the problem before they spend one hour understanding their options. I have seen taxpayers lose sleep, avoid opening their mail, and convince themselves that the IRS is going to take everything they own. Most of the time, by the end of the first meeting, they realize the situation is not nearly as hopeless as they thought.

That doesn’t mean the problem is easy. It doesn’t mean the debt disappears. It simply means there are often more options available than people realize.

The first thing we need to do is figure out where you are. How much do you owe? Have all the returns been filed? What is your income? What assets do you have? Once we know the facts, then we can start talking about solutions.

And there usually are solutions.

Installment Agreements

This is probably the most common solution.

Most people cannot write a check to the IRS for $20,000, $50,000, or $100,000. The IRS knows that.

In many cases they will allow you to make monthly payments over time. One of the most common arrangements is a payment plan that can extend as long as 72 months.

Is it perfect? No.

Interest usually continues.

Some penalties may continue.

But for many people it allows them to sleep at night because they know the problem is finally being addressed.

I’ve helped a lot of Idaho taxpayers establish installment agreements over the years. Sometimes the payment is larger than they expected. Sometimes it is smaller. Every case is different.

The important thing is getting the IRS under control and creating a plan that is manageable.

Offer in Compromise

This is the one everybody asks about because they have heard the commercials.

“Can I settle for pennies on the dollar?”

Maybe.

But maybe not.

An Offer in Compromise is designed for people who genuinely cannot pay the debt.

The IRS is going to look at your entire financial picture. They will review your income, expenses, assets, bank accounts, retirement accounts, real estate, and future earning potential. In simple terms, they want to know whether they believe they can collect the debt.

If they think they can collect it, the offer is probably not getting accepted. If they think they cannot, then an Offer in Compromise may be worth pursuing.

One thing I tell people all the time is that owing a large amount of money does not automatically qualify you for an Offer in Compromise. I know that’s not what people want to hear, especially after watching television commercials that make it sound easy.

I’ve had taxpayers come into my office owing $200,000 and not qualify. I’ve had others owing far less who did qualify. The difference is not always the amount of debt. The difference is the taxpayer’s ability to pay under IRS rules.

That’s why every case starts with the same thing: gathering the facts and doing the math.

Over the years, I have helped taxpayers in Boise, Meridian, Eagle, Garden City, throughout Idaho, and across the country settle IRS debts through this program. Some offers were accepted. Some were not.

I even had a client file bankruptcy in the middle of an Offer in Compromise. Needless to say, that changed the direction of the case.

The amount owed is only one piece of the puzzle. The real question is whether the IRS believes you have the ability to pay.

Currently Not Collectible Status

This is one that confuses a lot of people.

Sometimes taxpayers assume that if they cannot make payments, they automatically qualify for an Offer in Compromise. That is not always true.

I have seen situations where a taxpayer has equity in a home or other assets but does not have enough monthly cash flow to make payments. In those cases, the IRS may consider placing the account into Currently Not Collectible status.

The IRS reviews income and compares it to allowable living expenses under its financial standards. If there is simply no money left after those calculations, collection activity may be suspended.

Now, the debt does not disappear.

But it can provide breathing room.

I have seen this help retirees, people dealing with serious health issues, and taxpayers who are simply going through a very difficult financial period.

The key is properly preparing the financial information and accurately presenting the taxpayer’s situation.

Penalty Relief

This is probably one of the most overlooked areas of tax resolution.

Many taxpayers focus on the tax balance itself and do not realize how much of the debt is actually penalties.

The first option is called First-Time Penalty Abatement. A lot of taxpayers qualify and do not even know it exists. If you have generally been compliant, filed your returns, and maintained a good history with the IRS, you may qualify. Sometimes this can save thousands of dollars.

The second option is Reasonable Cause Penalty Relief.

Life happens.

People get sick.

Businesses struggle.

Family members pass away.

Divorces occur.

Natural disasters happen.

Over the years, I have worked on cases involving cancer, depression, alcoholism, caregiving responsibilities, and many other difficult life circumstances. When there is a legitimate reason why compliance became difficult, the IRS may consider penalty relief.

Not every case qualifies, but it is always worth looking at.

A Real-Life Observation

One thing I have learned after more than two decades of doing this work is that IRS problems rarely happen overnight.

Most tax debt grows slowly.

A missed payment becomes two.

A difficult year becomes several difficult years.

A taxpayer tells themselves they will catch up next year.

Then one day they wake up and owe far more than they ever imagined.

By the time many people walk into my office, they have spent months worrying about the problem. What often surprises them is that once we sit down and review the facts, there are usually more options available than they realized.

The fear is often worse than the first conversation.

I’ve had people drive all over Idaho to meet with me about an IRS problem. Often, after we finish the meeting, they say the same thing:

“I wish I had done this sooner.”

The IRS problem is usually not as bad as people imagine it to be on the drive to my office. Once you understand where you stand and what options are available, the fear starts to lose some of its power.

Don’t Wait Too Long

If there is one piece of advice I would give to anyone who owes the IRS, it is this:

Do not wait.

Most tax problems become more expensive over time.

The sooner you address the issue; the more options are generally available.

I know it can feel overwhelming. I know many people feel embarrassed or frustrated. But owing the IRS does not make you a bad person. It simply means there is a tax problem that needs a solution.

Every week I meet with taxpayers who are convinced there is no hope. More often than not, once we sit down, review the facts, and evaluate the available programs, we discover options they never knew existed.

Nobody has ever walked into my office happy to see me because of an IRS problem. But by the end of the meeting, most people are relieved because they finally understand what they are dealing with and what can be done about it.

Final Thoughts

Every tax situation is different, but in my experience, there is usually a path forward.

Sometimes the answer is an installment agreement. Other times it may be an Offer in Compromise, Currently Not Collectible status, penalty relief, or a combination of several solutions.

The worst thing you can do is nothing at all.

The best thing you can do is gather the facts, understand where you stand, and develop a plan.

After more than 15 years helping taxpayers resolve IRS problems, I can tell you that most people feel better after the first meeting because they finally understand their options.

If you owe the IRS more than you can pay, don’t assume there is no solution. There may be more options available than you realize.